What is Blockchain technology?

Recent remarkable price boom of Bitcoin creates an eagerness to find out more about this controversial digital currency. At the beginning of 2017, 1 Bitcoin price equals to around $1000 and by December of the same year, it was skyrocketed to high price as $18000. Experts believe that price of a Bitcoin will further rise over $100,000 in the future. Bitcoin was first introduced by a person or group of people known as Satoshi Nakomoto. In 2008, they published a white paper containing the technology of Bitcoin, which allows conducting peer to peer digital transaction without the third-party intermediary. Although the Bitcoin became a buzzword in the digital world, blockchain is the underlying technology of Bitcoin. Other than Bitcoin, today many other digital currency applications use the blockchain technology.

Before blockchain technology was introduced, digital transactions usually combined with trusted third parties (banks or financial institutions) and every transaction must undergo an authentication process, though this third-party involvement ensures the security, at the same time it increases the cost of the transaction. For an example, if you want to do a payment to the foreign company, trusted third party intermediary like a bank needs to facilitate that transaction. Banks usually charge some amount for the overseas transactions and it takes few days to complete the transaction. Blockchain excludes this third-party involvement and allows the fast and cost-effective way of a digital transaction between you and the foreign company. Authentication of the transaction through an intermediary is an essential part of the digital transaction, otherwise digital assets can be reproduced and use more than in one transaction. This issue is known as Double-Spending and this problem is common to digital currencies as well. Blockchain technology successfully eliminates the intermediary role and use a different mechanism to cope with issues like double spending.

The blockchain is a distributed electronic ledger which shared among disparate participants of the decentralized network. This electronic ledger contains the details of every transaction and all the data publicly available for all participants in the network. Distributed ledger is similar to a shared database, but each participant has their own copy of ledger and when a transaction takes place all ledgers simultaneously get updated. Transaction records entered to the distributed ledger are immutable, therefore participants can view the true records of every transaction and it also helps to avoid the frauds.

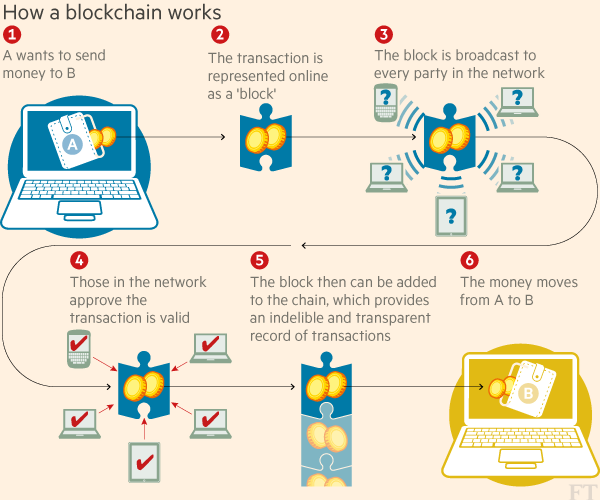

How does Blockchain work?

When a digital transaction begins, all the data linked to that particular transaction collects and creates a cryptographically protected unit called block in the blockchain network. Each participant in blockchain network refers to as nodes. Once the block is created, a message is sent to the entire network and special nodes called miners take interest on this new transaction. Miners, the computers with high level of computing power, then validate the transactions. These miners validate transactions by solving complex mathematical problems also known as puzzles, they use hashing algorithms to validate the block data and continue the process until it finds the correct solution. After the puzzle is solved, the miner who first validated the transaction publishes the validation logic. Other miners then check the accuracy of the solution and agree to that solution if the validation method is correct. Then the newly verified block is time stamped and will attach to the previously verified block and form a chain of blocks. This process gives highly traceable and transparent transaction flow. Miners who found the solution will be rewarded. (Bitcoin network rewards the miners with 25 Bitcoins per each solution).

Source: Financial Times

Mainly, two types of blockchain networks can be identified, namely public blockchain and private blockchain. Both blockchains allow a peer to peer transaction while maintaining a distributed ledger and transaction records entered into the blockchain are immutable. Anybody can join the public blockchain network and role of the intermediary is completely excluded in these types of blockchains. When a transaction takes place, entire network participates to validate the transaction, therefore public blockchains can ensure a higher level of security to the digital assets. Since the validation process takes substantial computational power, high energy supply requires to operate the public blockchains and speed is slower than private blockchains. Blockchain networks like Bitcoin, Litecoin and Ethereum can be recognized as public blockchains.

Individuals who granted permissions can access the private blockchain networks. Mostly, large organizations set up private blockchains to streamline their business processes. Compared to the public blockchains, these blockchains are providing fast and efficient environment to do transactions and ensure the high privacy level.

The benefits of Blockchain technology

Removal of intermediaries

When the Bitcoin was first introduced, one of the major objectives of blockchain technology is to eliminate the third party intermediary in digital transactions. Without an intermediary, two parties can establish a peer to peer transaction model and do transactions by minimizing the frictions in online businesses. In traditional transaction models, trusted third parties like banks, government, financial institutions are involved to validate the digital transactions and these third parties charge high fees to facilitate these transactions. By using consensus mechanism, blockchain excludes these expensive intermediaries and allows a cost-effective and fast way of transaction. In addition, consensus mechanism (proof of work in Bitcoin) provides a high degree of security to digital transactions than in traditional methods.

High security

Since all participants of blockchain network own a copy of distributed ledger, when transaction details enter to a particular ledger, all other ledgers of the network simultaneously get updated. Therefore, hackers attempt to corrupt records in one ledger become useless, they need to hack into every ledger in the network and it’s nearly impossible since it requires to hack thousands of computers. This is a great benefit which can gain through decentralized blockchain technology over centralized systems. It also helps to reduce the cost related to the security of the network.

Immutability and transparency

Data entered to the blockchain is almost impossible to alter again, therefore blockchain technology ensures the trustworthiness of its transaction. All the transaction details record in blocks and shared among participants, hence the transparency of transactions are high and it helps to create traceable systems.

Automation

Blockchain networks like Ethereum use Smart contract to automatically execute the set of rules for a business transaction without any third party involvement. Smart contract reduces the human intervention to the network and ensures the error-free running of digital transactions.

High speed

When a digital transaction goes through a third party verification process, it takes a long time to complete the transaction, as blockchains exclude the third party intermediaries and use new concepts like Smart contract, eventually, it reduces the transaction time to few minutes and allows the faster business process. Each participant of the blockchain network maintain a copy of the ledger, therefore data become highly available within the network.

Future of Blockchain technology

Blockchain technology has a potential to completely transform the existing business models and practices in online transactions. Excluding of intermediaries is a huge part of that process and it will revolutionize the global economy, therefore we can consider blockchain as a disruptive technology. Generally, banks facilitate online transactions as intermediaries, but in future, central banks also consider to adopt the blockchain technology in order to lower the settlement risk and efficient cross-border payment.

It’s predicted that, smart contracts will have a great effect on many areas of the future world, especially the areas like elections, logistics etc. Smart contracts are digitalized form of agreement or contract between associated parties and automatically executes relevant contract rules when a transaction takes place. Gartner, a research company, estimated that, by 2022 ratified unbundle (that is, defined impact) smart contracts will be in use by more than 25% of global organizations. Gartner has also predicted that, apart from the financial services, blockchains will change the other areas including government, healthcare, manufacturing, identity verification, supply chain etc.

Currently, a small proportion of global GDP stored in the blockchains. World Economic Forum (WEF) has stated blockchain technology as one of six megatrends in the future world, they predicted that, by 2025, 10% of global GDP would be stored on blockchains.

Don't forget to follow us on our social networks to keep track of all the latest blog posts!